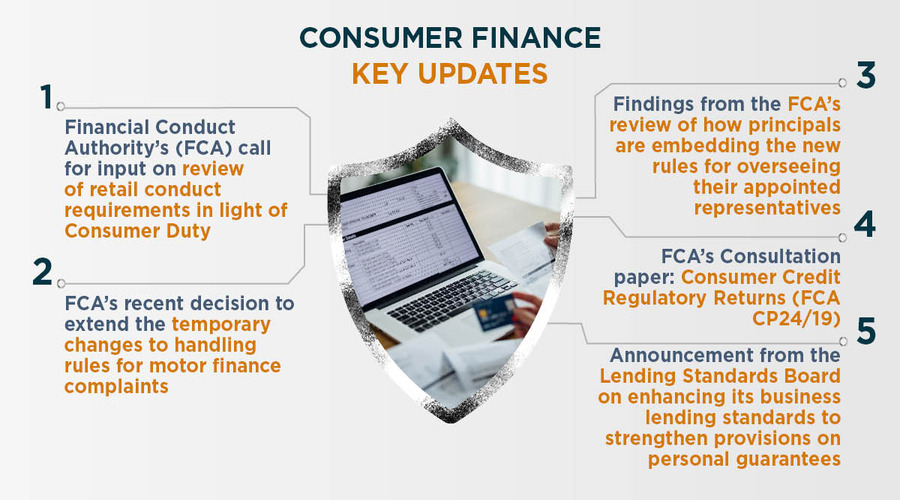

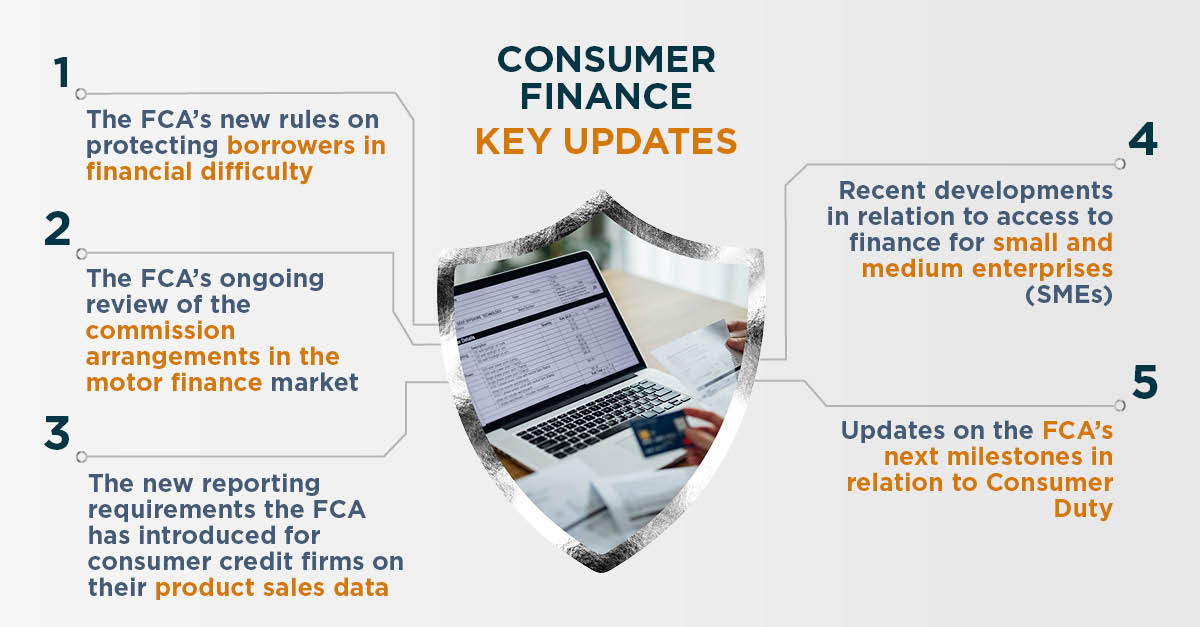

Customer redress and motor finance commission

Helping companies manage customer redress, including motor finance

The UK Financial Conduct Authority is emphasising the importance of proactive customer redress. The need for robust, dynamic, cost-effective redress delivery is greater than ever.

Motor finance commission is shaping up to involve a major FCA-led redress process. Responding will entail addressing legal complexity, managing litigation risk and delivering efficient, consistent redress outcomes. There may also be litigation claims brought outside of the redress arrangements.

We are currently advising motor finance lenders to prepare for the Supreme Court judgment in Hopcraft, forthcoming FCA redress plans, conduct customer redress and beyond, using our experience of regulation, FCA intervention, redress schemes and motor finance litigation.

Our experience has been built through supporting over 15 major banks and other financial services companies to manage redress effectively using our AI-enabled tech product, AG Remediate.

How our unique integrated approach and redress product will help you:

- Integrate your redress arrangements with litigation risk and complaints handling, under cover of legal privilege

- Devise and apply the right analysis with the right information

- Easily visualise progress, trends, plans and bottlenecks for sharing with your team, stakeholders and regulators

- Efficiently communicate good, timely customer outcomes

What is the product?

1

Combines our

legal & compliance expertise

Combines our legal and compliance expertise with AI to assess and deliver accurate, consistent and cost-effective redress outcomes.

2

Displays tailored

dashboards

The product shows case analysis, project progress and trends, and pinpoints exposure.

3

Stores all your

customer data

It also stores all your customer data and documents in one place, making information and analysis easy to find, and contacting customers quick and simple.

Helping companies manage motor finance litigation

For those outside of the redress scheme, either by choice or because they are not within scope, litigation may be pursued and encouraged by claims management companies (CMCs).

For a number of years, litigation has been on the rise in respect of motor finance commissions. As many will know, the majority of cases in this space are now stayed pending the outcome of the Supreme Court case of Hopcraft. As well as those outside of any redress scheme, there could be a further surge in litigation following the handing down of the judgment, which is expected in July.

How we defend lenders in respect of motor finance commission claims

- A seamless end to end service from complaint/ pre action stage through to final determination.

- Detailed strategic advice based our knowledge of how such cases are managed by CMCs

- Co-ordinated and collaborative teams of experts, calling on regulatory and contentious regulatory lawyers as required

- A highly skilled bank of junior lawyers who are trained on the issues and processes to conduct cases efficiently and at proportionate cost

- Tailored templates and precedents for the efficient management of mass litigation

- Advice in relation to attempted group litigation

- Technology driven solutions to increase efficiencies, drive down cost and provide you with automated MI

Recent examples of customer redress work for clients

Motor finance commission advice and read across

Advising several lenders and banks on the liability and risk implications arising from the Court of Appeal decision in Hopcraft, Wrench and Johnson, reviewing product arrangements and creating a risk rating tech tool.

Bank customer onboarding remediation

We conducted a legal, regulatory and customer experience remediation of business customer onboarding processes for a global bank using our AG Remediate platform to provide decisioning clarity, track workflows and accountability, surface legal gaps using AI and provide dynamic visual reporting.

Fraudulent investments

We advised a retail bank that had a large number of bank account customers who had invested in a fraudulent investment scheme, helping them to both assess and calculate redress for customers, and manage complaints that fell outside of the core redress programme, including several successful submissions to FOS to limit the scope of the bank's liability.

Private bank loans

We helped a private bank conduct a lending past business review and redress programme of over 300 consumer credit, regulated mortgage, and unregulated loan templates. We supported the bank by identifying and organising template and unique clauses and contracts, testing compliance of the operation of the loans against the contractual terms and regulatory requirements. We recommended appropriate redress where necessary in light of Ombudsman and regulatory redress approaches.

Retail banking – regulation and probate

We advised a major retail bank on a review of its treatment of deceased customers, designing a fair treatment programme in light of regulatory requirements and probate law, and supporting remediation wherever something had not gone right.

Key contacts

London

Leeds

London, UK