Partner, Co-head of Energy for Business, Energy and Utilities

United Kingdom

View profile

On 26 May the Department of Energy and Climate Change (DECC) published its long-awaited FIT review for Anaerobic Digestion (AD) and micro-Combined Heat and Power (mCHP). This follows on from the earlier review of the FIT scheme: see our article Happy New Year for FITs? for background.

The FIT scheme has encouraged more AD installations than the Government had originally projected. When it was launched in 2010, the Government predicted 100 AD installations would benefit, equating to 160MW of electricity, by 2020/21. In fact, by the end of March 2016, with five years still to go, there were 250 FIT-accredited AD installations or 177MW. This has prompted concern that if such growth continues, the spending cap on FIT subsidies under the Levy Control Framework will be exceeded.

The Government's response, as for other technologies in the FIT scheme, is to propose reducing the level of FIT payable and putting a cap on the number of installations that can accredit for FIT each quarter.

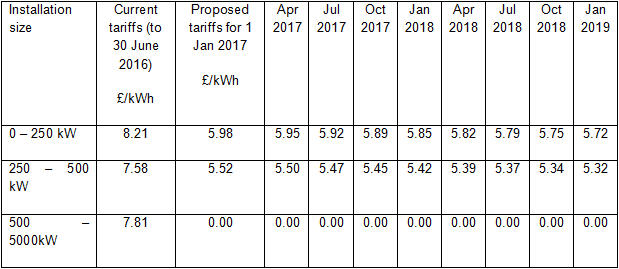

From January 2017, AD tariffs will reduce as shown in the table below. The (relatively) good news for AD installations under 500kW is that DECC propose to maintain the current tariff default degression trajectory, which means that tariffs will degress each quarter by 0.5% or 0.6% until March 2019 regardless of whether a deployment cap is reached. The table below shows what the tariffs would be under default degression.

The bad news is that AD installations of 500kW and over will no longer receive a generation tariff. According to DECC's tariff-setting methodology (which is bound to be disputed by the industry), AD installations that claim RHI payments, rely on 100% food waste as their feedstock and receive a gate fee of £20 per tonne should receive a 9.1% rate of return without FIT support.

In addition to the default degression, if a deployment cap is reached in any quarter, all subsequent tariffs will degress by a further 10% (contingent degression).

The deployment cap for AD in each quarter is 5MW, as mentioned in the previous FIT consultation. Ofgem publish a periodic FIT deployment caps report which shows how many installations have applied for FITs in any quarter, and the exact time (which depends on when the last application within a cap was submitted) a quarterly cap was reached. Applications that arrive after the cap is reached are then rolled over into the next quarter and start to fill up that quarter's cap. Once that is filled, they go into the next quarter, and so on.

Looking at the latest set of figures, as soon as the FIT scheme reopened on 8 February, the caps filled up. There are 27 AD projects currently queued and all the caps are filled up to Q2 2017. So any project applying now will probably have to wait 12 months before receiving FITs, and they will receive FITs at the new rates.

Projects that have already applied for preliminary accreditation but are above the cap and currently queued for Q1 2017 will have the new generation tariff rates applied to them. This affects 7 projects with capacities of between 100 and 800kW. Three of these are above 500kW so will potentially receive a tariff of zero.

The tariffs for mCHP will stay the same at 13.61p/kWh. However, support for mCHP will now be brought within the £100m Levy Control Framework budget by using underspends from the other technologies. This means that underspend that might have been recycled by topping up deployment caps is now being spent on mCHP.

To control the level of spending on mCHP, the Government is introducing a deployment cap of 3.6MW to March 2019, in the form of annual caps of 1.6MW in each of 2017 and 2018 and 0.4MW to the end of March 2019.

If an annual deployment cap is reached, it will trigger a 10% contingent degression on the tariffs for subsequent years.

Introducing these caps means that mCHP will never become more than a pilot; the FIT will not enable a mass roll-out. In reality, the low take-up of mCHP may mean that the caps are not reached as long as the pace of installations continues at its current rate; there have only been around 650 installations up to now.

DECC are proposing to introduce sustainability criteria to new AD installations from January 2017. They recognise that many AD projects apply for both the RHI and the FIT and so want to make the sustainability criteria consistent.

The FIT sustainability criteria will apply to a new AD installation unless it is/becomes RHI accredited too, in which case the RHI criteria will apply instead.

The FIT sustainability criteria are:

a) Land criteria:

and

b) Greenhouse gas (GHG) emissions limit: every consignment of feedstock must meet a minimum standard of 66.7gCO2e/MJ of electricity generated, falling to 55.6 from 1 April 2020 and then 50.0 from 1 April 2025.

Feedstock made up wholly of waste does not have to comply with either of these.

Failure to meet these criteria in any quarterly reporting period means an installation is not entitled to FITs for that period.

As for the RHI (see RHI Reforms 2016), DECC are proposing two options for restricting payments for electricity generated from biogas that is derived from feedstock that is not waste or residues, to discourage AD installations that use all or mainly crops as feedstock.

Option 1 is that FITs are only payable for electricity generated from biogas derived only from wastes and residues

Option 2 (the preferred option) is that FITs are payable on 50% of total biogas yield, for electricity generated from biogas not derived from wastes and residues.

DECC are planning for these measures to be in place by January 2017, although the feedstock restrictions will come into force when the RHI ones do. Once the measures are in force they will affect installations that are granted full or pre-accreditation after that. Existing installations are not affected.

The consultation closes 7 July and in its Response DECC will give more detail of when the proposals will be implemented. The Anaerobic Digestion and Bioresources Association is already preparing a strong response so DECC will have much to digest before making a final decision.